As part of the OBBBA (you can read our full write-up on it here), the enhanced senior deduction was added as a provision to fulfill President Trump’s promise of no tax on Social Security benefits. While it doesn’t quite eliminate the tax on Social Security benefits, it does provide a significant tax savings and planning opportunity for those over 65. Now that we’ve had a full tax year working with clients to navigate this, here’s how to best maximize the deduction.

Key Takeaways:

- The enhanced senior deduction is an additional deduction for those over 65 that stacks on top of their standard deduction

- Management of your AGI is important to manage the enhanced senior deduction and the phaseout can cause higher effective rates

- It can make sense to convert past the deduction depending on your situation and balancing the tax savings now vs. the future is an important distinction

The Enhanced Senior Deduction

The One Big Beautiful Bill, passed in 2025 was a sweeping tax bill that added numerous new provisions and phase outs to the tax code. One of those was the “Enhanced Senior Deduction”.

Taxpayers over age 65 with an AGI below $75,000 (single) or $150,000 (MFJ) receive the full $6,000 deduction per qualifying taxpayer — stacked on top of the standard deduction. The deduction phases out at six cents per dollar above those thresholds, disappearing entirely around $175,000 (single) and $250,000 (MFJ). In 2026, the base standard deduction is $16,100 (single) / $32,200 (MFJ), plus an additional $2,050 for single filers age 65 or older, or $1,650 per qualifying spouse for MFJ filers.

So in 2026, a single filer age 65 or older starts with a total standard deduction of $18,150. A married couple where both spouses are 65 or older gets $35,500 ($32,200 + $1,650 x 2). That’s a pretty good start! Add the enhanced senior deduction and those figures climb to $24,150 (single) and $47,500 (MFJ, both 65+). Remember, in retirement that deduction “eats up” your first dollars of pension income, IRA withdrawals, or taxable Social Security — effectively making that income tax-free. It’s one of the biggest reasons effective tax rates for retirees are so low.

One of the biggest opportunities or considerations is that this deduction for now, is temporary. It is slated to expire December 31, 2028. So, what we have here is a temporary reprieve on taxes for retirees. The good news for those over 65 is this is one of those things that becomes really popular and politically unpalatable to repeal.

Does the Enhanced Senior Deduction eliminate taxes on my Social Security?

I get this question a lot. As you can see above, the enhanced senior deduction is just another deduction stacked on top of deductions that you already earn as a tax filer. According to the White House, 64% of filers over 65 and receiving Social Security benefits have deductions that exceed taxable Social Security income.

With the enhanced senior deduction added to the mix, that number jumps to 88%. For most retirees, their total deductions now simply exceed the portion of Social Security that’s subject to tax in the first place — effectively making it tax-free income. Worth noting though: the deduction isn’t targeted specifically at Social Security. It reduces your overall taxable income, and Social Security just happens to benefit along with everything else. So while it doesn’t technically eliminate the tax on benefits, for most retirees over 65, the practical effect is pretty close.

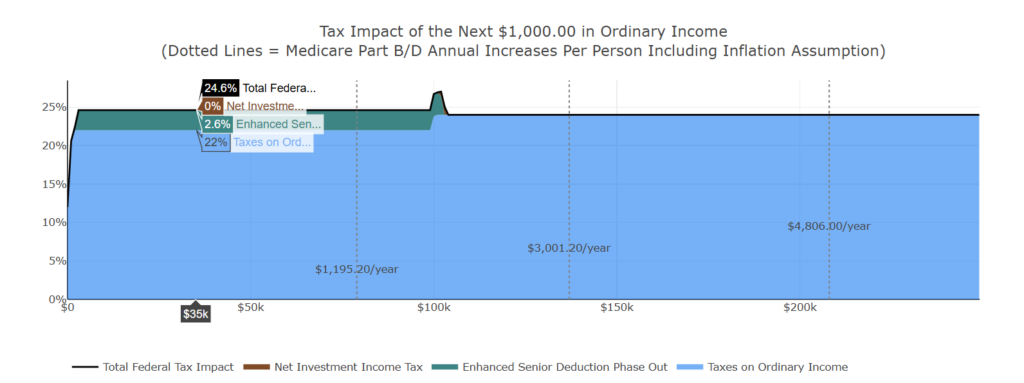

The Phaseout Trap: How One Extra Dollar Can Cost You More Than You Think

The biggest opportunity is preserving the full deduction. The income level to preserve the deduction has a phaseout range. So, if you earn a dollar over the limit, not only do you pay a tax on that dollar but a dollar that was previously non-taxable becomes taxable. This increases the marginal rate. You can see a graphic of this dynamic below.

Let’s walk through an example. It’s worth noting that the Enhanced Senior Deduction income limitation applies to your AGI, or gross income. For a couple who are both 72, with $150,000 in AGI, will preserve the full $12,000 deduction. However, in the next year they’ll be required to take a required minimum distribution of $10,000.

That will put their AGI for the following year at $160,000 – all else being equal. Two things happen, first the dollars of their RMD are taxed at 22%. The $150,000 in AGI less the new deduction fills up the 12% tax bracket. The additional RMD not only is taxed at 22%, but also it causes a loss of $1,000 of the enhanced senior deduction. So the actual tax is $2,200 (22%*$10,000) but also (22%*1,000) so $220. The effective tax of the RMD is $2,420/$10,000 despite only being in a 22% bracket. That’s an extra 2.4% higher than it has to be.

Sometimes there isn’t much you can do with an RMD, you have to take it. But this is a great time to discuss whether a Qualified Charitable distribution (QCD) might be appropriate to satisfy your RMD and not have any of that income fall on to your 1040.

Thinking about Roth IRA conversions

The first principle of tax planning is paying taxes when you believe they’ll be low to you. Roth IRA conversions are an imperfect science as we can only make a best guess at what rates might be in the future. Things like RMDs, life expectancy, tax policy, asset returns will all affect whether a partial Roth IRA conversion works out, or doesn’t.

If we continue our example above, the couple in the 12% bracket who is capturing the full enhanced senior deduction. Additional dollars withdrawn or converted would fall not only in the 22% bracket, but have an effective tax of 24.6% due to the effect of the deduction also phasing out. In 4 years, this couple will have to take RMDs – the year after the enhanced senior deduction expires. Taken a step further, their financial plan forecasts their RMDs will never get large enough to push them out of the 22% bracket (it’s pretty wide!).

If these clients were to convert this year, they’d pay 24.6% on the dollars they converted (up to the full phaseout of $250k in AGI). However, assuming the enhanced senior deduction isn’t renewed, would only be paying 22% federal income tax on their RMDs. Does it make sense to pay 24.6% to avoid 22% in tax? The answer is probably not.

What many people get wrong about Roth IRA conversions is that it isn’t about the growth — it’s about the tax you’re electing to pay. The savings is the additional dollars that get to compound in your portfolio. If you’re paying more now to avoid a lower tax later, you’ve handed more dollars to the government than you had to.

When It Makes Sense to Convert Anyway

As I mentioned, the future is impossible to predict with any specificity. So in 4 years, could we have a new set of marginal tax rates that are higher? Yes. In that case, a 24.6% tax rate may be cheap. It can be as much art as science.

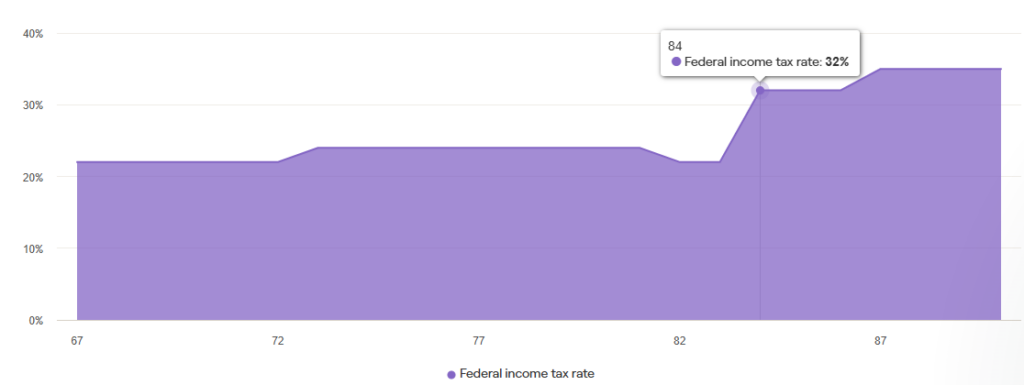

Two more common examples where it can make sense to ditch the enhanced senior deduction is planning for the widow’s penalty as well as prioritizing legacy goals. Below is an image of a marginal tax rate increase later in life due to a “widow’s penalty”. Going from 22% to 35%! That might be worth avoiding.

The widow’s penalty occurs when one spouse predeceases the other and the surviving spouse moves into paying single rates. Assets still pass to one spouse so RMDs are required, and more often than not the compressed rate tables cause a higher marginal rate. It isn’t uncommon for a married couple in the 22% bracket to find the surviving spouse in a 32% bracket. Of course this depends on your unique circumstances. The larger your IRA balance and the age spread between spouses, the more pronounced this penalty may get.

Non-spouse IRA beneficiaries also have to distribute inherited IRAs (except in certain cases) over a 10 year period. This can make the case for doing some lifetime gifting or Roth IRA conversions if the children are high income individuals in their own right. They’ll have to distribute the IRA on top of their earned income. For those parents who are reading this saying “who cares they are lucky to get an inheritance”, I hear you. That said, it’s still more money that your family will end up paying in tax.

Let’s say your children are a doctor and an attorney. On their return this year, they’ll each have $250,000 in taxable income as single filers. If the kids each receive half of a $1,000,000 traditional IRA ($500,000 each), they’ll have to deplete those assets over 10 years. On their own, each child is in the 32% marginal tax bracket, meaning every dollar of IRA income they receive gets taxed at 32% federal. Does it make sense to convert some of your IRA at 24.6% — even at the cost of losing part of your deduction — to save at least 7% in taxes? I think of it as a guaranteed 7% return on the taxes you pay today. It’s a strategy that keeps more money in your family. How much you care about improving an inheritance is a personal decision, but the end result is the same: the government gets less.

In Summary

The enhanced senior deduction is one of the more meaningful, and underused planning opportunities we’ve seen added to the tax code in a while. Quite frankly, I see a lot of advisors skimming right over it. For retirees in the right income range, it quietly reduces your tax bill every year it’s in effect. But it also changes the math on decisions you may already be thinking about: when to convert, how much to convert, and whether your current strategy still makes sense in light of it.

What makes this deduction different from a typical tax break is that it interacts with nearly every other lever in a retirement income plan. Your RMDs, your Social Security taxation, your Roth conversion strategy, and your legacy goals all run through the same AGI number that determines whether you keep the full deduction or start giving it back dollar by dollar. That’s why it can’t be evaluated in isolation and why a quick back-of-the-napkin estimate often misses the real opportunity.

The right answer looks different for everyone. A couple with modest RMDs and no pressing legacy concerns probably wants to stay inside the deduction as long as possible and let the tax savings compound quietly. A couple with a large IRA, a significant age gap, and high-earning kids may find that selectively converting past the deduction, even at a higher effective rate today produces a better outcome for the family over time. Neither approach is universally correct. What matters is running the numbers on your specific situation before defaulting to one strategy or the other.

The window runs through 2028. That’s three more years — but the clock is already running on the first one. If you haven’t mapped out how the deduction fits into your broader plan, that’s exactly the kind of thing we work through with clients. Reach out for a free Retirement Review and we’ll show you where you stand.