Let’s pick up where we left off – funding investment accounts for your kids or grandchildren. If you haven’t read the first part of our giving blog series, I’d recommend going back and starting there. You can jump there by clicking here.

Key Takeaways

- UTMA accounts can be a simple tool to give money to a minor with limits on control.

- Kiddie tax can mean investments have a tax liability equal to the parents

- Trusts can provide control but may have significant ongoing cost and tax liabilities

Uniform Transfers to Minors Act

The Uniform Transfer to Minors Act (UTMA) is a law passed in 1986 that allows adults to transfer assets to a minor (under the age of majority – age 18 for most states) without need for a formal trust. A UTMA account is not a trust, but is an investment account with an owner, and a minor beneficiary.

When I talk with clients about transferring assets to children, and a 529 feels too confined, the next option is usually a UTMA. A UTMA does not have the “rules” or limitations about use when it comes to withdrawals.

However, without any caveats upon use, there are no tax benefits and in fact there may be unintended tax liabilities as a result (we’ll talk about the kiddie-tax later).

How a UTMA Works

For parents who want to fund an investment account for a minor – a UTMA account is opened. The account is funded and can be invested in a wide number of assets. UTMA accounts replaced their UGMA predecessors and as a result can hold a number of types of assets such as stocks, bonds, real estate, and other assets depending on the custodian.

The UTMA will be opened in the name of the custodian for the benefit of the minor. This is important – the amount funded into the UTMA is an irrevocable gift. So, the property that has entered the account is now the property of the beneficiary.

The account and its assets will be held and invested until the beneficiary reaches the age of majority (click here to view states ages of majority). Upon the beneficiary reaching the age of majority, the assets must be turned over to the beneficiary. Again, for most states this is the age of 18.

A Blunt Instrument

We don’t have to write too much on the technicalities of a UTMA. It’s quite simple. Simplicity in financial planning can cut both ways. While a well-funded UTMA may grow significantly over 18 years, it may also mean an 18-year-old has full control over that pool to do as they now please. I’ve seen parents attempt to “not tell” beneficiaries about these assets – and in recent years custodians have become stricter on making sure assets are distributed once the minor reaches the age of majority. After all, it is their money.

The real question is how capable your 18 year old beneficiary may or may not be in having access to such a pool of capital. There are no limitations to their withdrawals and use of the funds. Matter of fact, due to the irrevocable nature of the gift, it’s extremely unlikely you could prevent such access.

This may sound like I’m dissuading you from using a UTMA, far from it. I just often caution the use of such instruments as it is incredibly difficult to predict where children’s financial sense may or may not be at age 18. I hope my own children are far more adept than I was!

Tax benefits – or lack thereof

UTMA’s because of their flexible nature lack any qualified or tax-preference status. So, they in essence enjoy the same tax benefits as your standard brokerage account (none), but do enjoy a much more liquid source of capital than say, a 529.

For clients who have a taxable brokerage account or revocable trust, you receive a 1099 annually that shows dividends, interest, and capital gains each year. The same will happen with a UTMA account.

Remember, you have made an irrevocable gift to the beneficiary. So, who bears the tax responsibility for the tax liability generated by the investments within the account? The beneficiary. And you might say, well they are 5 and they don’t need to file a return!

Reasons your minor will file a return

You can read here IRS publication 929 on Tax rules for Children and Dependents. Also here is a link to filing requirements for dependents. Generally, there are a few reasons your minor may have to file a return:

- Employment Income in excess of the standard deduction ($14,600 for 2025)

- Unearned income in excess of $1,300 for 2025 (unearned being interest and dividends from say, a UTMA account!)

- Owing Medicare or Social Security tax on wages or tips not reported

- Alternative Minimum Tax

- Distributions from an HSA or 529

- Self employment income of $400 or more

- Taxes withheld and they want to claim a refund

The Kiddie Tax

We’re going to focus on item #2 from above – unearned income as it applies to children under 19 (or 24 if a full time student). The first $1,300 of unearned income – dividends, interest, capital gains in a child’s name are tax-free. The next $1,300 is taxed at the child’s rate (typically 10%) and then anything over is taxed at the parents rate!

So, in essence, you have a child’s investments being taxed at the parents rate. This can be problematic for high earning parents or grandparents and creating additional tax drag on the performance of the investments over time.

If the child’s unearned income is less than $11,000, parents may opt to include it on their own tax return using form 8814. However, that would require a special set of circumstances as most often it would mean even higher taxes.

What about a Trust?

Thus far we have only reviewed investment accounts set up by a custodian for a minor beneficiary. As you can see, the tax benefits and limits vary significantly. One of your last options is a trust. We’ll likely have an entire separate blog on trusts we’ll cover some briefly here.

Trusts generally fall into two buckets: Revocable and Irrevocable. Revocable means the money is still yours. Money can flow in and out, you can change the terms, so forth and so on. Usually there is no separate entity or tax ID. This type of trust wouldn’t constitute a “gift” to a minor given the control you still retain.

An irrevocable trust is the opposite. It is a completed transfer and is a separate entity. You may have limited powers to change things, but for all intents and purposes the money has been given away. It will also more than likely have its own tax ID and require a separate tax return.

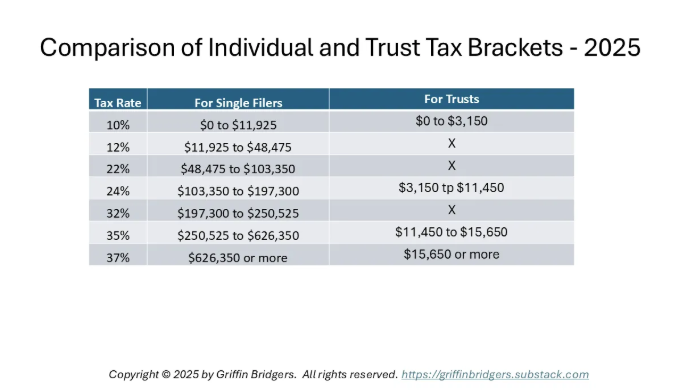

Irrevocable is a strong word – and in the case of an irrevocable trust it should be. Your choice is generally irrevocable. As would be a gift to a UTMA. Trusts and Estates also have their own tax rates. The rates are the same as an individual payer, but the brackets are compressed significantly. You can see an example below:

It doesn’t take much income from a trust (only $16,000) to find yourself in the top tax rate. See the tax brackets below from Griffin Bridges.

Is the juice worth the squeeze?

On top of the punitive tax brackets, the illiquidity, cost to set-up (attorneys fees) can be daunting for most households. Arguably though, an irrevocable trust provides the most control over how the disposition of the assets may work.

Say you don’t want access to funds until the age of 30, or want to limit creditors accessing the funds. Such stipulations are often found in a trust for gifting to a minor.

In Summary

The options of giving money to your children, grandchildren, or the next generation are varied. We have significant expertise and experience in such conversations and making sure your family has the best options of transferring wealth and getting the next generation started on the right foot.

If you have questions, give our free retirement review a shot. We’re glad to offer you insights on how best these strategies may fit into your planning.